Socially driven

Inclusive financial services

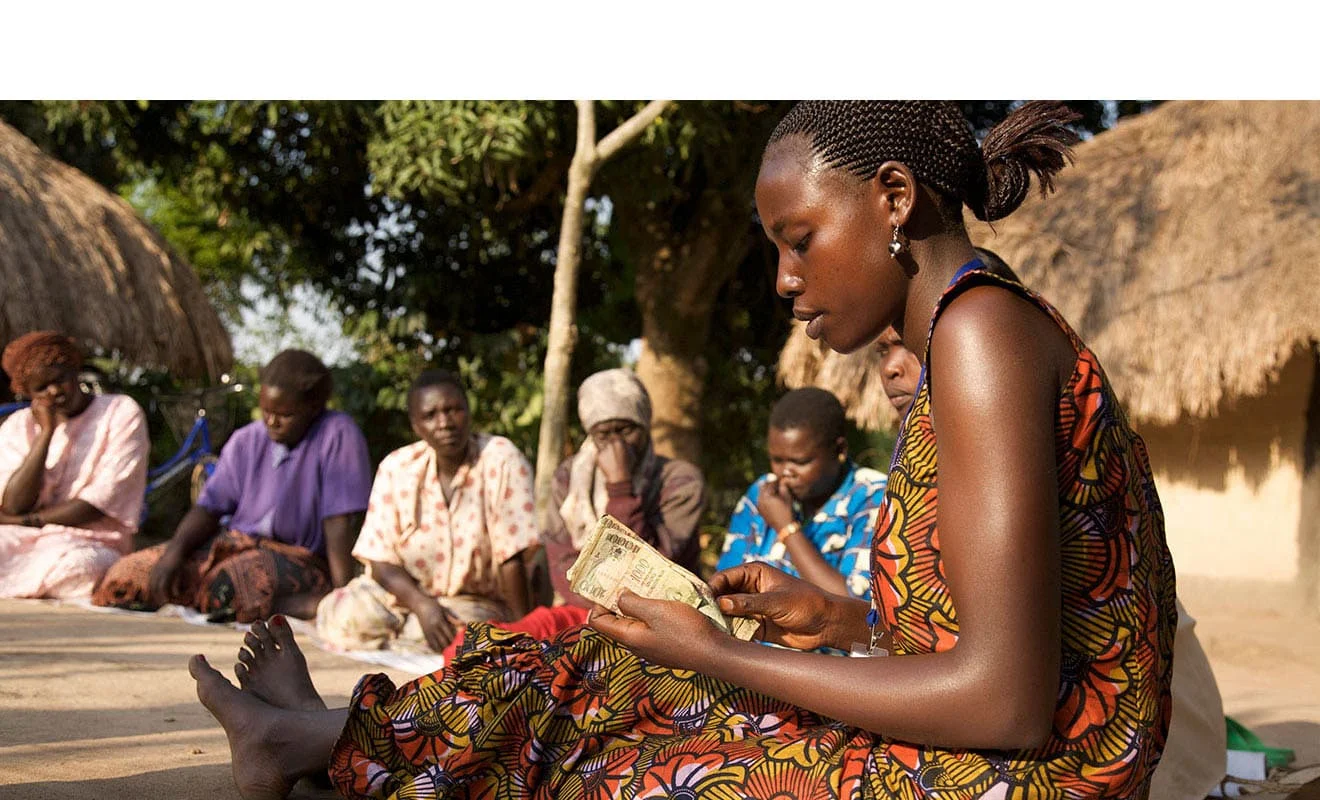

Empowering women

Digital innovation

Holistic approach

Socially driven

Socially driven

To create a positive impact in the lives of our clients is our only bottom line. We deliver financial services in a way that is transparent, fair, and safe, adhering to the Universal Standards for Social Performance Management and the Client Protection Principles, placing clients’ well-being at the center of everything we do to achieve our mission.

Inclusive financial services

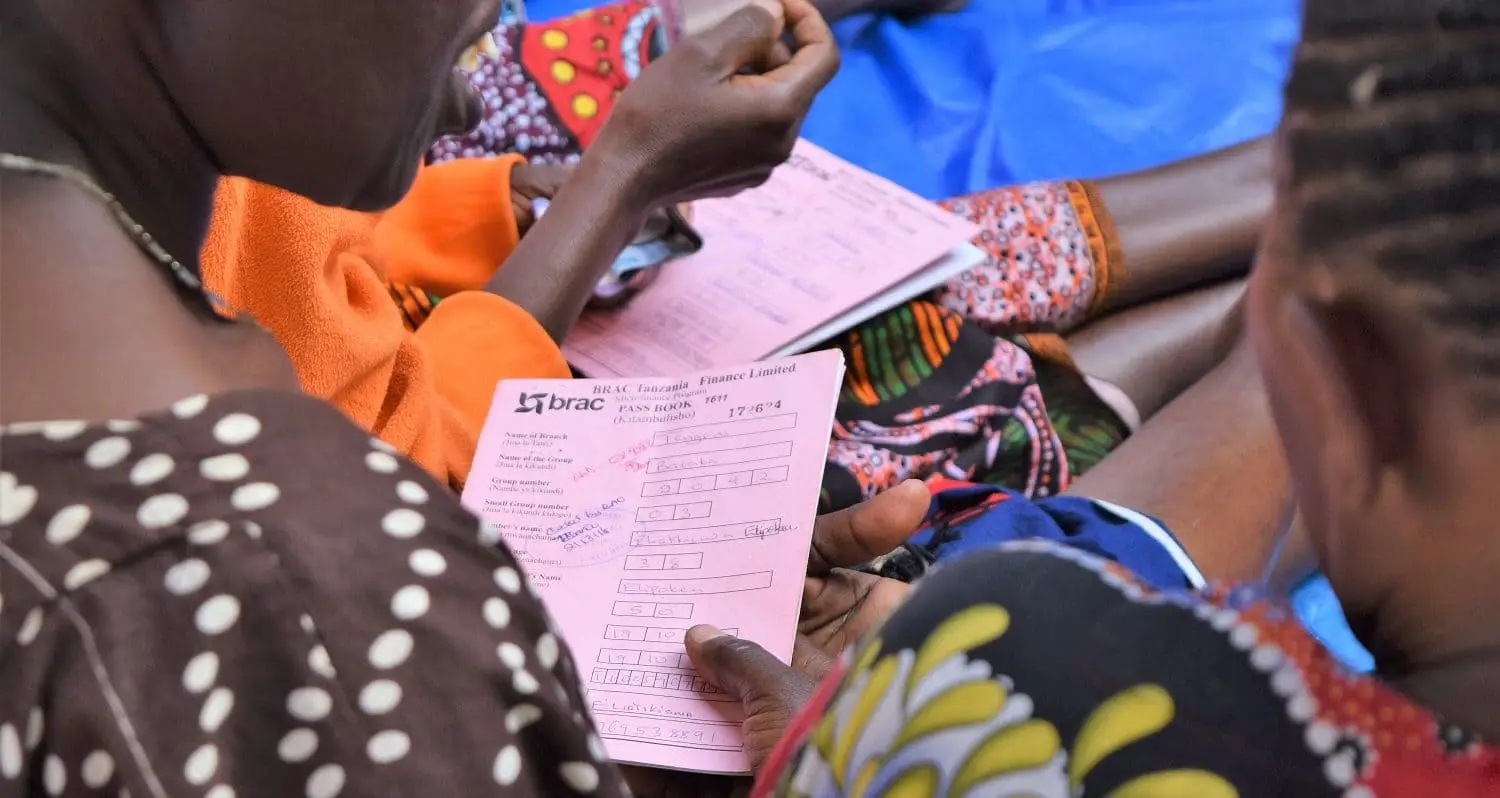

Inclusive financial services

We offer inclusive, accessible, and convenient loan and savings products tailored to the needs of the local community, including women, smallholder farmers, small business owners, and youth. We complement these services with financial literacy training, enabling borrowers to make informed financial decisions.

Empowering women

Empowering women

When women have control of their finances, they are more likely to invest in family needs, such as health care, nutrition, and education for their children. We primarily focus on women, enabling them to become financially resilient and improve the quality of life of their families.

Digital innovation

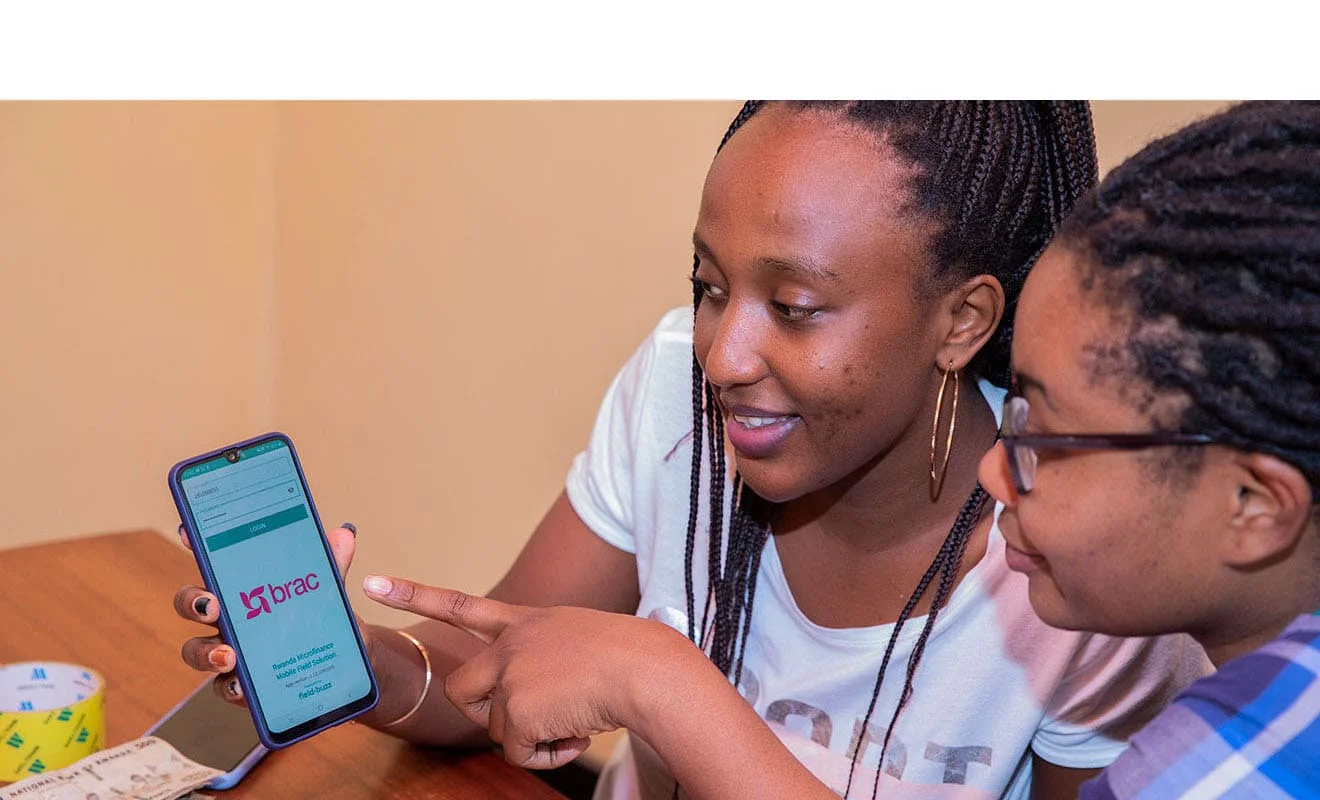

Digital innovation

The client value proposition is at the core of our digital transformation efforts, with a particular emphasis on reducing the gap in women’s digital financial inclusion. We are embracing financial technology by digitising field operations and adopting alternative delivery channels to increase operational efficiency and offer greater convenience to our clients.

Holistic approach

Holistic approach

Pairing microfinance with other social services can amplify the impact of our mission. We complement our microfinance services with many of our social development programmes, such as youth empowerment, agriculture and food security, and livelihood programmes.

Myanmar

Tanzania

Uganda

Rwanda

Sierra Leone

Liberia

Ghana

Myanmar

Myanmar

BRAC Myanmar Microfinance Company Limited was launched in 2013. It provides inclusive financial services to people living at the bottom of the pyramid, with a strong focus on women living in rural and hard-to-reach areas, and marginalised populations. With 85 branches in 83 townships of the country, it has the third largest branch network among all microfinance operators in Myanmar.Read More →

Tanzania

Tanzania

Founded in 2006, BRAC Tanzania Finance Limited is the largest microfinance institution in Tanzania in terms of branch network, active borrowers, and loan outstanding. Across 162 branches, it provides access to finance to people living in poverty, focusing particularly on women living in poverty in rural and hard-to-reach areas.Read More →

Uganda

Uganda

BRAC started microfinance in Uganda in 2006, as a part of BRAC Uganda’s social development programmes. It transformed into a Tier 2 Credit Institution to become BRAC Uganda Bank Ltd in 2019. BRAC Uganda Bank Ltd has the largest network of banking services in the country, providing inclusive financial services for low income communities to build sustainable livelihoods.Read More →

Rwanda

Rwanda

Having launched microfinance operations in June 2019, BRAC Rwanda Microfinance Company PLC seeks to provide financial services responsibly to people at the bottom of the pyramid. It is the first BRAC International microfinance entity to launch as a deposit-taking institution and fully digitised operations from the outset. Currently, a total of 35 branches have been established in 18 districts, serving 25K borrowers, 98% of whom are women.Read More →

Sierra Leone

Sierra Leone

BRAC Microfinance Sierra Leone Limited is the largest microfinance institution in Sierra Leone with 42 branches in 12 districts, 60K borrowers, and a loan portfolio of over USD 25.2 million. It provides inclusive financial services to people living in poverty, with a strong focus on women living in rural and hard-to-reach areas.Read More →

Liberia

Liberia

Launched in 2008, BRAC Liberia Microfinance Company Limited is the largest microfinance institution in Liberia, operating with 45 branches in 7 counties. It provides inclusive financial services to people living in poverty, with a strong focus on women living in rural and hard-to-reach areas.Read More →

Ghana

Ghana

BRAC Ghana Savings and Loans Ltd and loans was launched in 2023. It is the seventh microfinance entity of BRAC International Holdings B.V. alongside six other microfinance institutions in Liberia, Sierra Leone, Tanzania, Rwanda, Uganda and Myanmar.Learn more →